Your credit score changes from time to time, and the frequency of changes may vary depending on your financial situation. It is calculated from the information in your credit report, which should be updated when there is any change. Your credit report contains information about your credit accounts, payment history, total available credit, and recent requests for credit.

Credit bureaus will receive information

Your credit score can change as credit bureaus receive information about lenders, credit card companies, and other businesses. These companies are legally required to report accurate information to the bureaus in a specific amount of time. Your score is then calculated by each bureau based on the most current information.

If you notice a mistake on your credit report, you can dispute it. The letter you send must contain a copy to the creditor indicating the dispute. The process of resolving disputes can take anywhere from 30 to 90 days. Most states will give you a free copy your credit report once it's completed.

Late payments

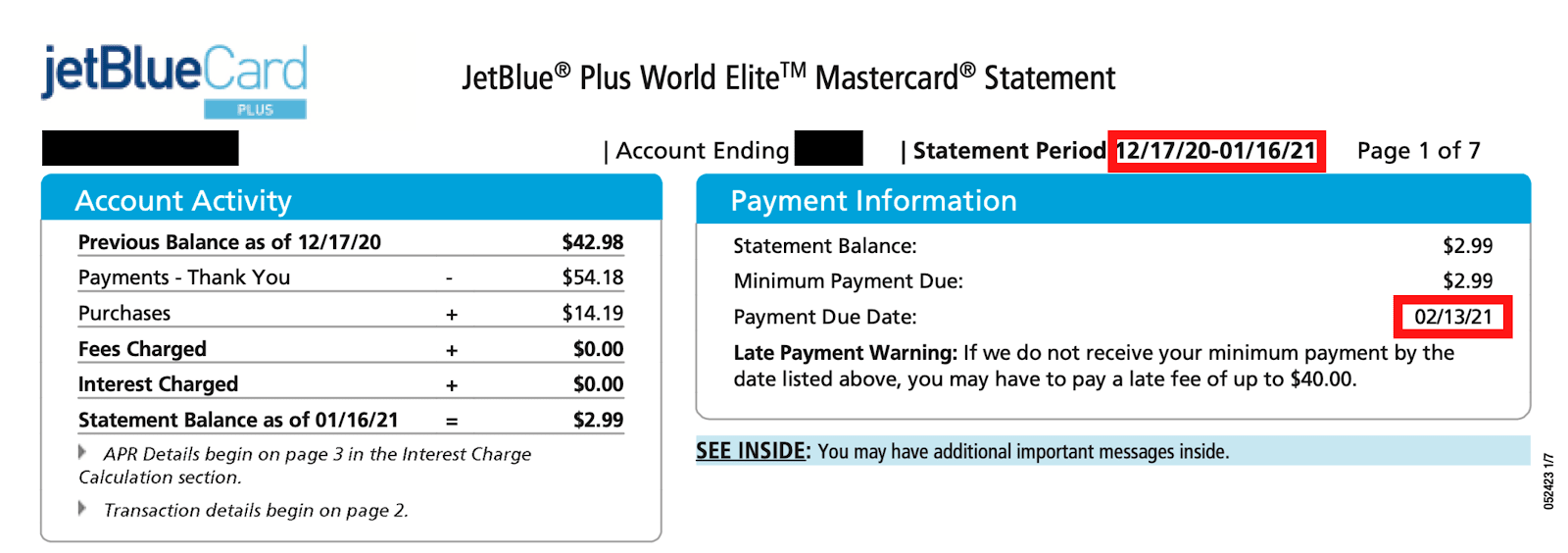

Late payments can damage your credit score. Late fees can be costly. However, you can take steps to avoid them. You can avoid them by paying your bills on-time. Late payments are reported to the credit bureaus at least 30 days after the due date. This gives you the opportunity to make up any missed payments. Late payments may also lead to an increase in your interest rate or a reduction of credit available.

Depending on the length of the delinquency, late payments affect your score differently. Your score will drop significantly if your payment is late for more than 30 days.

Hard inquiries

You may be most concerned about the number and nature of hard inquiries that are on your credit report. While the number of hard inquiries is not as important in calculating your credit score but they play an important role in assessing your likelihood of repaying your debts, Your income and payment history are all factors that lenders look at when pulling your credit card report. You could be at higher risk of defaulting if you have too many difficult inquiries on you credit report.

One inquiry can bring down your credit score five points. However, a combination of two or more can result in a 10 point drop in your credit score. People who have six or more previous hard inquiries are eight times as likely to file for bankruptcy. The good news? Most people don't need as many inquiries in order to adversely affect their scores.

Lenders can report account and payment information

Credit scores update every month when new information from creditors is reported to the credit bureaus. Some lenders may report information less frequently than others. This means that if you pay off a debt, it may not appear on your credit report immediately. This can mean that your payment may not appear on credit reports for 30 to 60 days.

Lenders must report information about account and payment to credit bureaus at the very least once per month. However, this can vary. Lenders report to only one or two bureaus monthly, while others report to all three. Most lenders report account information and payment information every month to the major credit agencies.